Fed Rate Cut Imminent: Markets Navigate Shutdown Chaos and Trade Tensions |

Market Sentiment Overview

Markets face unprecedented uncertainty as the US government shutdown enters its 24th day—the second-longest in history—delaying critical economic data releases. The Federal Reserve is virtually certain to cut rates by 25bps on Wednesday despite limited visibility into economic conditions. Gold corrected sharply from record highs above $4,380 after a 5.3% single-day plunge, while stocks set fresh all-time highs on easing inflation. Trump and Xi Jinping’s meeting at the APEC Forum in South Korea could determine whether the fragile US-China trade truce extends beyond November 10.

Currencies

USD Index: Consolidation Amid Shutdown Uncertainty (99.00)

Current Trend: Consolidative/Mixed Market Sentiment: Uncertain

The US Dollar navigated choppy waters, closing modestly higher around 99.00 despite marking its fourth consecutive monthly decline—down nearly 10% since February’s tariff-driven peaks. The Greenback’s direction remains clouded by the ongoing government shutdown, which has halted most economic data releases except for September CPI. With the Fed’s 25bps rate cut on Wednesday virtually certain (markets pricing 100% probability), focus shifts to Chair Powell’s guidance on the December meeting. The court battle over Trump’s tariff authority adds another layer of uncertainty, with appeals ongoing after a lower court blocked “Liberation Day” tariffs.

Potential Resistance: 99.20; 100.04

Potential Support: 98.10; 97.33

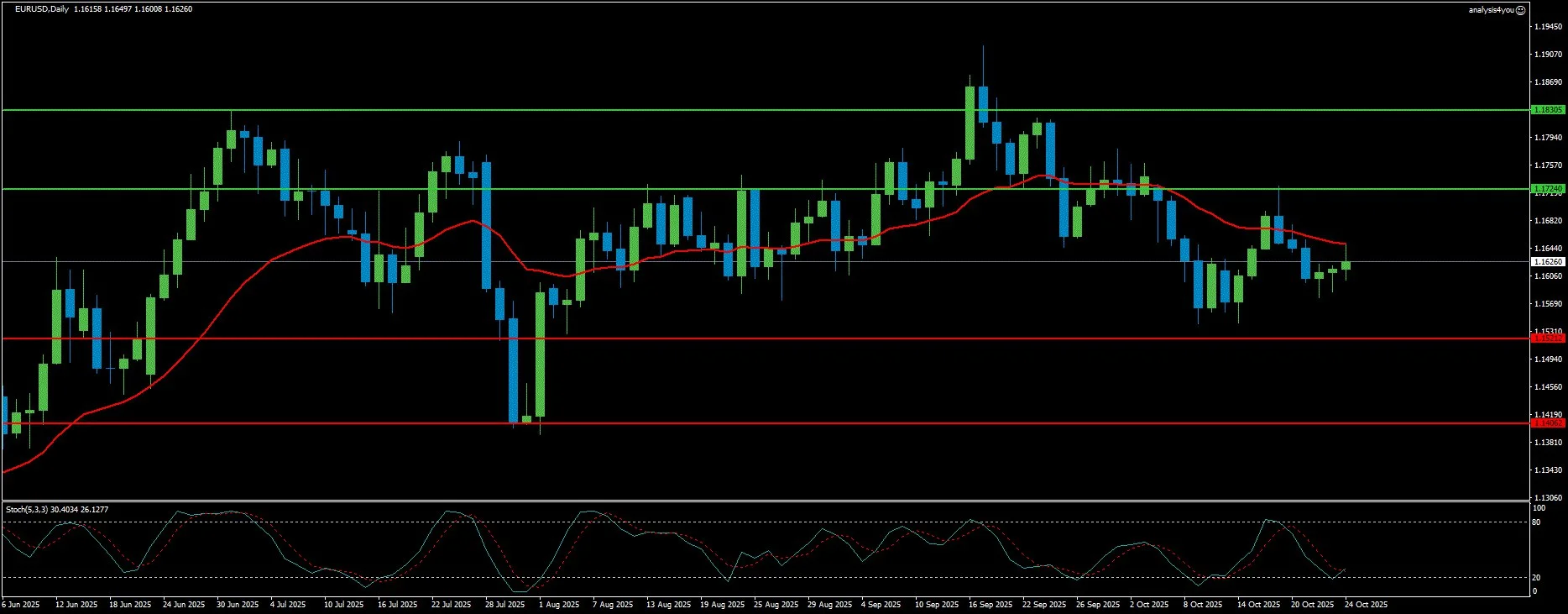

EUR/USD: Gearing Up for Dual Central Bank Decisions (1.1620)

Current Trend: Bearish (Near-term) Market Sentiment: Cautious

EUR/USD ended the week with modest losses around 1.1620, trading below both the 20-day and 100-day SMAs amid fading upside momentum. The pair faces critical tests from both the Fed (Wednesday) and the ECB (Thursday) meetings. While the Fed is expected to cut 25bps, the ECB has explicitly stated comfort with current rates and no plans for near-term action, creating policy divergence pressure on EUR. German Q3 GDP and October HICP data will provide additional directional cues.

Potential Resistance: 1.1724; 1.1831

Potential Support: 1.1521; 1.1406

GBP/USD: Sellers Return as BoE Cut Bets Rise (1.3280)

Current Trend: Bearish Market Sentiment: Negative

GBP/USD reversed sharply from near 1.3500, falling back toward 1.3280 after softer UK inflation data boosted December rate cut probabilities to 61% from 46%. The September CPI held steady at 3.8%, versus the expected 4.0%, triggering profit-taking after the Pound’s strong run. Despite positive retail sales (+0.5% in September) and improved PMI data (51.1 vs 50.6 expected), bearish momentum intensified.

Potential Resistance: 1.3438; 1.3553

Potential Support: 1.3197; 1.3071

Stocks

S&P 500: Record Highs on Strong Earnings, Fed Dovishness (6,770)

Current Trend: Strongly Bullish Market Sentiment: Optimistic (But Stretched)

The S&P 500 surged to fresh all-time highs, gapping up on Friday after softer CPI data sealed expectations for Wednesday’s Fed rate cut. With 29% of companies reporting Q3 earnings, 86% have beaten estimates, driving blended earnings growth to 9.2% year-over-year (above initial 7.9% expectations). The index now stands 20% above its April 7 low, but it shows a rising wedge pattern formation—often a bearish reversal signal.

Potential Resistance: 6907.47; 7046.27

Potential Support: 6694.91; 6566.95

Magnificent 7: Five Report Earnings This Week

Current Trend: Mixed Market Sentiment: Anticipatory

Five of the Magnificent 7 report this week: Alphabet (GOOGL), Meta (META), and Microsoft (MSFT) on Wednesday; Apple (AAPL) and Amazon (AMZN) on Thursday. These companies are critical—they drive outsized S&P 500 earnings growth and serve as bellwethers for AI boom sustainability. Tesla (TSLA) already disappointed, declining after missing estimates. With 173 S&P 500 companies scheduled to report, management’s forward guidance will be scrutinized heavily, given the shutdown’s impact on economic visibility.

Potential Resistance: 453.39; 469.28

Potential Support: 413.21; 396.45

Commodities

Gold: Sharp Correction After Record High (4,100)

Current Trend: Corrective/NeutralMarket Sentiment:Uncommitted

Gold staged its largest one-day loss of 2025 (down 5.3%) after hitting a record high of $4,381 on Monday, snapping a nine-week winning streak. The correction to $4,100 was driven by improving risk appetite on easing US-China trade tensions and profit-taking after the extended rally. Technical indicators show Gold returned to its six-month ascending channel with RSI dropping below 60, highlighting a loss of bullish momentum. The Xi-Trump meeting at APEC is crucial—failure to extend the trade truce beyond November 10 could reignite safe-haven demand.

Potential Resistance: 4247.27; 4378.61

Potential Support: 3959.13; 3828.92

WTI Crude Oil: Surges on Russia Sanctions, Supply Fears (61.50)

Current Trend: Bullish Market Sentiment: Positive

WTI crude jumped 7.6% for the week to $61.50, while Brent climbed to $65.94, driven by fresh US sanctions on Russia’s two largest oil producers (Rosneft and Lukoil). The sanctions shifted supply risk from theoretical to tangible, potentially tightening seaborne flows. Serbia’s NIS refinery disruption after a US waiver expired adds to supply concerns, threatening 80% of Serbia’s fuel supply. Despite US crude inventories falling 2.8 million barrels (more than expected), RBOB gasoline remains subdued at $1.923, suggesting limited pass-through to consumers yet.

Potential Resistance: 63.67; 66.10

Potential Support: 59.25; 56.83

Crypto

Bitcoin: Reclaims $111,000 Despite Institutional Caution (111,000)

Current Trend: Consolidative Market Sentiment: Mixed

Bitcoin recovered to $111,000 after finding support at the 61.8% Fibonacci retracement level ($106,453), but faces critical tests. “Dolphin” holders (100-1,000 BTC wallets)—comprising ETFs, corporations, and large holders—control 26% of the circulating supply, but their buying has slowed. Glassnode warns that BTC trading below the short-term holders’ cost basis at $113,100 indicates growing demand exhaustion. Institutional flows remain indecisive, with spot ETFs alternating between inflows and outflows. Positive catalysts include Trump’s pardon of Binance founder CZ and Bealls Inc. becoming the first US national retailer to accept crypto payments.

Potential Resistance: 117990.65; 121619.51

Potential Support: 109859.31; 106097.65

Central Bank Calendar & Key Events (October 28 – November 1, 2025)

Major Central Bank Meetings

- Wednesday, October 29: Federal Reserve (25bps cut to 3.75%-4.00% range virtually certain)

- Wednesday, October 29: Bank of Canada (expected to hold at 2.50%)

- Thursday, October 30: European Central Bank (expected to hold at 2.00%)

- Thursday, October 30: Bank of Japan (expected to hold at 0.50%)

Key Economic Releases

- Monday: Dallas Fed Manufacturing Index

- Tuesday: Conference Board Consumer Confidence, S&P/Case-Shiller Home Prices

- Wednesday: MBA Mortgage Applications, EIA Crude Oil Inventories

- Thursday: German Labor Market Report, Germany & Eurozone Q3 GDP (advance), Germany & Eurozone October HICP

- Friday: Chicago PMI, Germany Retail Sales, Eurozone Unemployment Rate

High-Level Diplomatic Events

- October 30 – November 1: APEC Forum in South Korea

- Critical Meeting: Trump-Xi Jinping summit to discuss trade truce extension beyond the November 10 deadline

Week Ahead Outlook

The coming week is dominated by three major themes: the Fed’s “cut in the dark” without recent employment data due to the shutdown, the critical Trump-Xi meeting that could determine trade relations through year-end, and a flood of Magnificent 7 earnings that will test AI boom sustainability.

Fed Decision:

With the 25bps cut fully priced, Chair Powell’s press conference becomes the main event. Markets will parse every word for clues on December’s path. Any hawkish tilt citing “elevated uncertainty” could support the Dollar and pressure Gold. Conversely, concerns about shutdown impacts on the labor market could validate another December cut (currently 92% priced).

US-China Trade:

The November 10 truce deadline looms. If the Xi-Trump meeting fails or is cancelled, expect safe-haven flows into Gold and Yen. Success could extend the risk-on rally in stocks but pressure precious metals. China’s proposed rare earth export controls and Trump’s threatened 100% tariffs add urgency.

Earnings Gauntlet:

Five of the Magnificent 7 report in 48 hours (Wed-Thu). With the group responsible for outsized index gains, disappointments could trigger broader market reassessment. Management guidance will be critical given the economic data blackout.

Government Shutdown:

At 24 days and counting, impacts are intensifying. If it reaches November 5, it will become the longest ever. Each additional week shaves GDP growth, increasing pressure for resolution but also clouding Fed decision-making.

Risk management is paramount given elevated volatility from central bank decisions, critical trade negotiations, earnings concentration risk, and ongoing political dysfunction in Washington. The technical setup in equities shows warning signs (rising wedge, extended valuations), while Gold’s sharp correction suggests even safe havens aren’t immune to profit-taking after extended runs.

Remember: In an environment where the Fed is cutting rates in the dark, Trump and Xi hold veto power over risk sentiment, and the government remains shuttered, position sizing and stop discipline matter more than directional conviction.