Dollar Extends Rally: CPI Data and Fed Speakers Take Center Stage

Market Sentiment Overview

The US Dollar extends its winning streak into a second consecutive week, climbing toward the key 99.00 level and building momentum for further gains. Markets are recalibrating after December’s weak NFP (+50K vs 60K expected) was offset by a lower unemployment rate (4.4%), keeping Fed rate-cut expectations muted. Tuesday’s CPI inflation data emerges as the week’s critical catalyst, while intensifying geopolitical risks in Venezuela, Iran, and around the Strait of Hormuz continue to support safe-haven demand. The S&P 500 hit fresh all-time highs above 6,968, signaling continued equity strength despite rising yields.

Currencies

USD Index: Building Momentum Toward 99.00 (98.81)

Current Trend: Bullish Market Sentiment: Positive

The US Dollar Index posted its second consecutive weekly gain, currently trading at 98.81 and approaching the psychologically significant 99.00 barrier. A break above this level would open the door for further advances toward the November 2025 peak at 100.39, and potentially the May 2025 high at 101.97. The Greenback’s strength comes despite mixed December jobs data, as markets interpret the 4.4% unemployment rate decline as evidence that the labor market remains firm enough to keep the Fed on hold. Tuesday’s December CPI report is the week’s main event, with markets watching closely for any signs that inflation remains sticky above the Fed’s 2% target. Fed officials remain divided on the rate path, with some calling for aggressive cuts while others stress restrictive policy should stay in place longer.

Potential Resistance: 99.49; 100.04

Potential Support: 98.22; 97.67

EUR/USD: Bearish Momentum Accelerates (1.1632)

Current Trend: Bearish Market Sentiment: Negative

EUR/USD tumbled for a second straight week, settling around 1.1640 and flirting with five-week lows near 1.1600. The pair faces mounting selling pressure as the Dollar strengthens and policy divergence widens between the Fed and the ECB. Europe’s economic progress remains tepid, with the Eurozone’s December Services PMI at 52.4 and Composite PMI at 51.5, both at three-month lows. ECB Vice President de Guindos stated current interest rates are “adequate,” signaling policymakers are done with rate moves for now, leaving the Euro vulnerable to continued Dollar strength. The pair has room to extend its decline toward the 1.1470 area if Dollar demand prevails.

Potential Resistance: 1.1702; 1.1781

Potential Support: 1.1544; 1.1468

GBP/USD: Deep Correction Underway (1.3400)

Current Trend: Bearish (Corrective) Market Sentiment: Cautious

GBP/USD extended its correction for a second consecutive week, breaking below the key 1.3400 level. The pair plummeted from four-month highs of 1.3568 as the USD resurgence and simmering geopolitical tensions weighed heavily. Safe-haven demand for the Greenback amid the US-Venezuela conflict and Iran unrest has exerted additional downside pressure on the risk-sensitive Pound. Wednesday’s UK monthly GDP data and Thursday’s Industrial and Manufacturing Production figures will be crucial in determining whether the longer-term bullish bias remains intact or if a deeper correction is ahead.

Potential Resistance: 1.3497; 1.3626

Potential Support: 1.3297; 1.3183

USD/JPY: Breaking Above 158.00 (157.90)

Current Trend: Bullish Market Sentiment: Positive

USD/JPY surged markedly this week, breaking above the 158.00 barrier for the first time since January 2025. The pair benefits from widening rate differentials as the Fed maintains its cautious stance. At the same time, the Bank of Japan remains trapped in ultra-loose policy due to Japan’s massive debt burden. The carry trade remains highly attractive, and any dips are being bought aggressively. Geopolitical tensions are failing to provide the traditional yen safe-haven support as traders focus on the overwhelming yield advantage favoring the Dollar.

Potential Resistance: 159.03; 160.09

Potential Support: 156.85; 155.69

Stocks

S&P 500: Record Highs Continue (6,962)

Current Trend: Bullish Market Sentiment: Positive

The S&P 500 closed Friday at a fresh record high of 6,966.28, up 0.65% on the session and 1.6% for the week. The index also notched a new all-time intraday high during the session at 6,968.42, marking the third time this week the broad market reached new peaks. The Dow Jones Industrial Average jumped 2.3% for the week to close at a record 49,504.07, while the Nasdaq Composite gained 1.9%. Despite weak December payrolls data (+50K), markets interpreted the lower unemployment rate as a sign the economy remains resilient, supporting continued equity gains. Homebuilder stocks surged after Trump directed representatives to buy $200 billion in mortgage bonds to drive rates lower.

Potential Resistance: 7041.34; 7119.39

Potential Support: 6849.17; 6778.60

Commodities

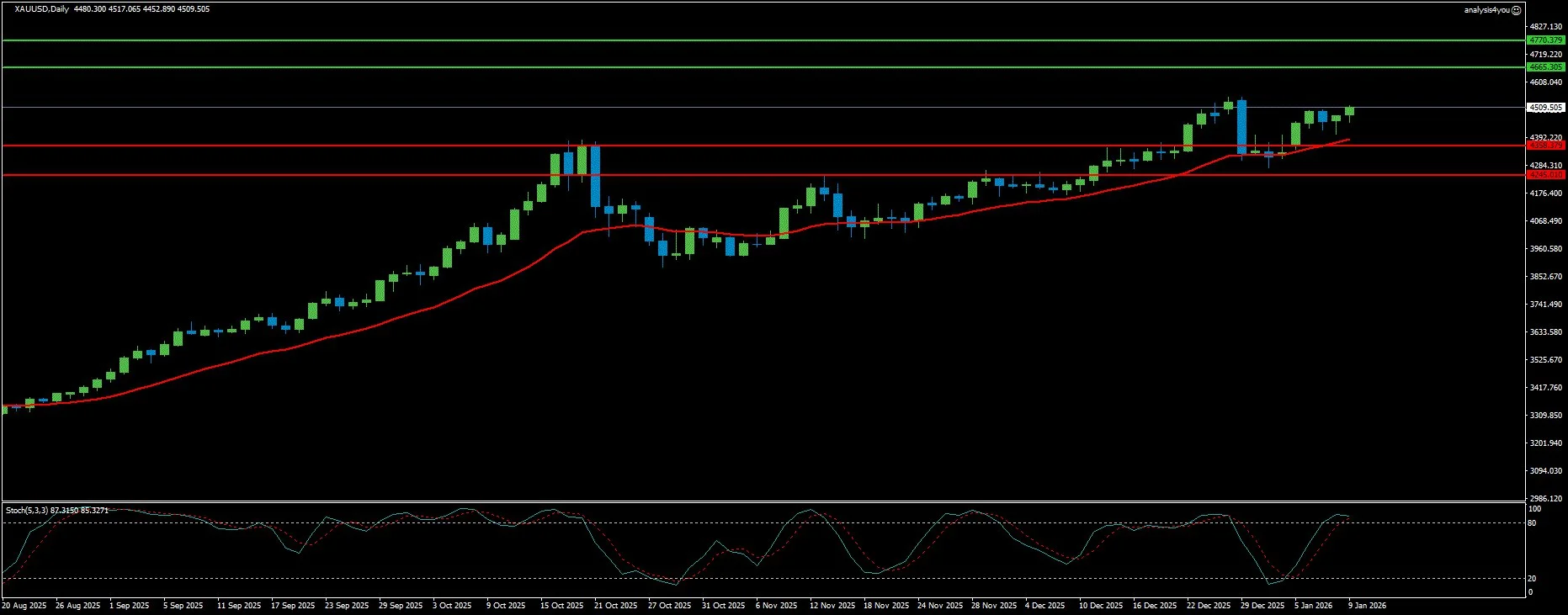

Gold: Testing $4,500 Amid Geopolitical Turmoil (4,510)

Current Trend: Bullish Market Sentiment: Positive

Gold rocketed above $4,500 per troy ounce, challenging yearly highs and posting a 4% weekly gain despite a firmer Dollar and rising US Treasury yields. The precious metal capitalized on intensifying geopolitical risks, including US military action in Venezuela, widespread protests in Iran, and Russian missile strikes on Ukraine. Risk-off sentiment continues to favor gold as a safe haven, with traders watching for any escalation in Middle East tensions or disruption to oil flows through the Strait of Hormuz. The bullish technical outlook remains intact, with momentum indicators supporting further upside potential.

Potential Resistance: 4665.30; 4770.38

Potential Support: 4358.38; 4245.01

WTI Crude Oil: Geopolitical Premium Returns (58-59)

Current Trend: Bullish Market Sentiment: Cautiously Positive

WTI crude climbed approximately 3% for the week to settle near $58-59 per barrel, while Brent gained 4% to reach $61-63. Oil markets are rebuilding geopolitical risk premiums following US military action in Venezuela, Trump’s plan to purchase 30-50 million barrels of sanctioned Venezuelan oil, and escalating unrest in Iran. Venezuelan production fell to 830,000 bpd in December, down 130,000 bpd from November due to US sanctions. However, fundamental oversupply concerns remain, with OPEC production steady around 29 million bpd and global inventories still rising. The market is trading the near-term instability rather than the longer-term supply normalization.

Potential Resistance: 60.20; 62.14

Potential Support: 56.85; 54.84

Crypto

Bitcoin: Institutional Outflows Pressure Price (90,000)

Current Trend: Bearish/Consolidative Market Sentiment: Cautious

Bitcoin continues trading near $90,000 after encountering rejection at key resistance zones, with the price pullback supported by fading institutional demand. US-listed BTC spot ETFs recorded net outflows of $431.02 million through Thursday after three consecutive days of withdrawals totaling $1.12 billion. Despite strong corporate demand (Strategy Inc. added 1,287 BTC, bringing the total to 673,783 BTC), the market structure suggests Bitcoin needs to clear heavy sell-side pressure between $92,100 and $117,400 before a sustainable rally can resume. Analysts warn that without clearing these distribution zones, BTC remains vulnerable to testing the $85,000-$86,000 support area.

Potential Resistance: 96510.75; 101361.41

Potential Support: 85462.02; 80543.99

Key Events This Week (January 12–16, 2026)

Critical Data Releases

- Monday: ISM Manufacturing PMI (December)

- Tuesday: US CPI Inflation (December) – Week’s Main Event

- Wednesday: US Retail Sales (November), PPI (October & November), UK Monthly GDP

- Thursday: UK Industrial & Manufacturing Production, US Weekly Jobless Claims, Existing Home Sales

- Friday: US Industrial Production, Manufacturing Production, Germany Full Year GDP

Central Bank Meetings

- Tuesday: Bank of Korea Rate Decision (2.50% expected)

- Wednesday: Polish Central Bank (NBP) Meeting (4.00% act vs 4.25% exp)

- Thursday: ECB Accounts Release

Fed Speakers (Through Week)

Extensive Fed commentary expected with Bostic, Barkin, Williams, Musalem, Paulson, Miran, Kashkari, Barr, Jefferson, and Bowman all scheduled to speak. Markets will parse remarks for clues on the January 28 meeting stance.

Geopolitical Flashpoints

- Venezuela: White House meeting Friday with oil executives on investment plans; Trump seeks to control oil revenue

- Iran: Escalating protests, internet blackouts, and Strait of Hormuz closure threats

- Greenland: Trump–Denmark tensions over potential US acquisition

- Russia–Ukraine: Continued missile strikes targeting energy infrastructure

Week Ahead Outlook

Tuesday’s December CPI report dominates the weekly calendar and could significantly impact the Fed’s policy path. Markets are watching for any signs that inflation remains sticky above target, which would support the dollar and justify continued Fed patience on rate cuts. A reading of 0.3% or higher on monthly core CPI could revive concerns and boost USD, while a softer-than-expected print below 0.2% might pressure the greenback. The technical breakout in the US Dollar Index above its 200-day SMA suggests momentum favors further gains, with the path now open toward the 100.39 level and potentially the May 2025 peak at 101.97.

Geopolitical risks remain elevated and asymmetric. Venezuela’s oil sector restructuring, Iran’s internal unrest, and potential Strait of Hormuz disruptions could drive significant volatility in energy markets and safe-haven assets. Oil’s current $58-63 range masks substantial tail risks, with analysts modeling Brent scenarios as high as $90-110 if major supply disruptions materialize.

Equity markets continue to show resilience despite rising yields, with the S&P 500’s record closes suggesting investor confidence in economic growth acceleration. However, strategists warn that breaking above 6,000 (already surpassed) may prove challenging if geopolitical tensions escalate or inflation proves stickier than expected.

Risk management remains essential given the potent mix of critical inflation data, extensive Fed commentary, elevated geopolitical tensions across multiple theaters, and technical breakouts in the Dollar that could accelerate if confirmed by supportive CPI data.