Fed Independence Under Fire: Powell Probe and Next Chair Speculation Dominate

Market Sentiment Overview

Political drama overwhelms markets as criminal charges against Fed Chair Jerome Powell spark unprecedented uncertainty about central bank independence. The Dollar posted its third consecutive weekly gain despite the controversy, while speculation intensifies over Powell’s successor, with Kevin Hassett emerging as Trump’s apparent favorite.

December CPI data met expectations but remained sticky at 2.7% YoY, reinforcing the Fed’s patient stance. Geopolitical tensions eased slightly as Trump stepped back from Iran’s military threats after assurances that killings would stop, providing mild relief to risk sentiment.

Markets now await critical PCE inflation data on Thursday and January PMIs on Friday, while the Davos Economic Forum brings global policymaker speeches throughout the week.

Currencies

USD Index: Political Uncertainty Fails to Derail Rally (99.50)

Current Trend: Bullish Market Sentiment: Mixed/Cautious

The US Dollar Index extended its winning streak for a third consecutive week, pushing decisively back above 99.00 and briefly touching six-week highs at 99.50. The rally persisted despite unprecedented political turmoil after the Department of Justice threatened criminal indictment against Fed Chair Powell over cost overruns in the Fed headquarters renovation. Powell fired back, describing the probe as a “pretext” to gain leverage over interest rate decisions and a consequence of Trump’s anger over the Fed’s refusal to cut rates more aggressively. Global central bank chiefs rallied in solidarity, stating, “Independence of central banks is a cornerstone of price, financial and economic stability.” The controversy raises profound questions about Fed independence, yet markets continue pricing in virtually no chance of a January rate cut (less than 5% probability). Thursday’s PCE inflation data and Friday’s PMI readings will be critical catalysts.

Potential Resistance: 99.49; 100.04

Potential Support: 98.51; 97.87

EUR/USD: Dull Trading Despite Political Drama (1.1600)

Current Trend: Bearish Market Sentiment: Negative

EUR/USD fell to a fresh January low of 1.1593, closing the week barely above 1.1600 despite broad USD weakness from the Powell controversy. Sellers successfully defended the upside around 1.1700 for a second consecutive week, leaving the pair trapped in a painfully narrow range. European data provided little direction, with Germany’s Q4 GDP rising 0.2% (from -0.5% revised) and Eurozone Sentix Investor Confidence improving to -1.8 from -6.2. Industrial Production rose 0.7% MoM in November. The ECB’s Lagarde will speak at Davos this week, while the calendar includes the final Eurozone HICP for December, German PPI, and the ZEW Economic Sentiment survey. The pair remains vulnerable to further downside toward the 1.1470 area if Dollar demand persists.

Potential Resistance: 1.1687; 1.1748

Potential Support: 1.1511; 1.1444

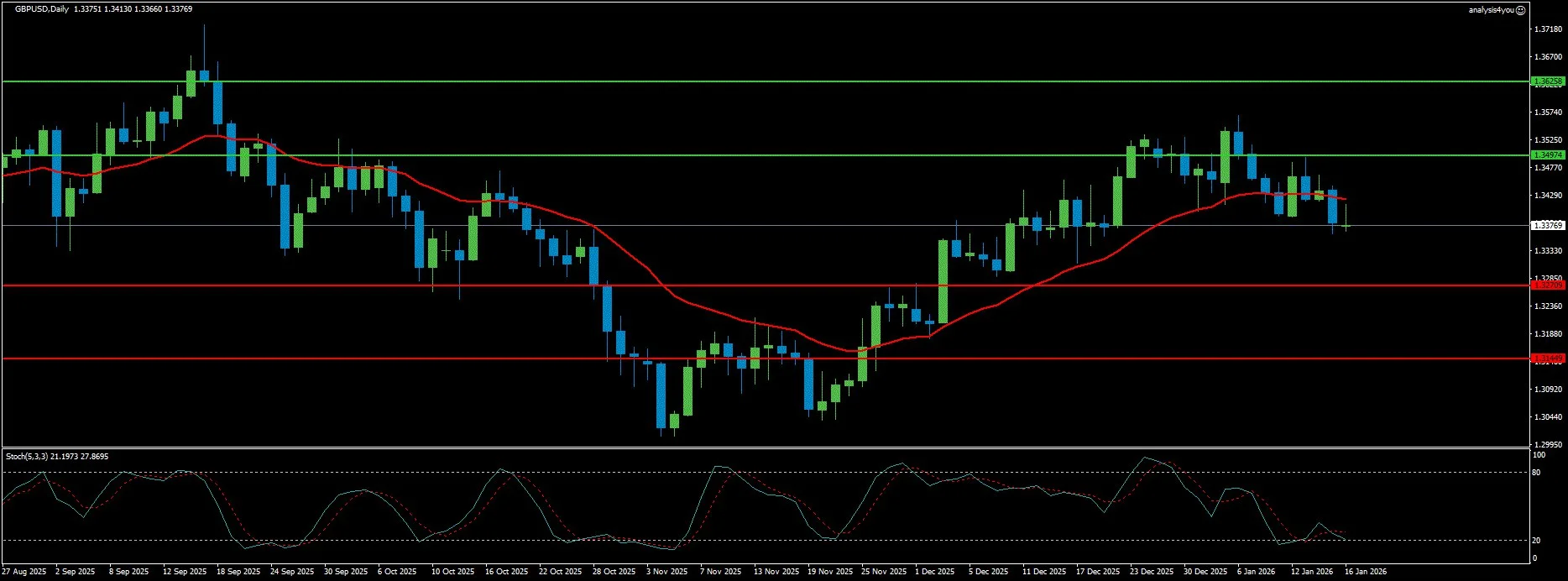

GBP/USD: Testing Four-Week Lows (1.3360)

Current Trend: Bearish Market Sentiment: Under Pressure

GBP/USD declined to four-week lows around 1.3360 after briefly jumping to 1.3486 on Monday following the Powell probe announcement. The pair turned down steadily as BoE policymaker Alan Taylor delivered dovish commentary, suggesting inflation could return to the 2% target in mid-2026 more quickly than expected and that interest rates could “normalise to neutral sooner rather than later.” Despite strong UK November GDP growth of 0.3% (vs 0.1% expected) and robust Industrial Production (+1.1% MoM) and Manufacturing Production (+2.1% MoM), the Pound failed to sustain gains. Tuesday’s UK employment data for the three months ending in November and Wednesday’s December CPI will be critical for determining the BoE’s February 5 policy decision.

Potential Resistance: 1.3497; 1.3626

Potential Support: 1.3271; 1.3145

Stocks

S&P 500: Market Concentration Risks Intensify (6,926)

Current Trend: Mixed/Cautious Market Sentiment: Concerned

The S&P 500 closed Friday down 0.5% at 6,926, pulling back from record highs as concerns mount about extreme market concentration. A mere 41 AI-related stocks now account for 47% of the index’s total value, creating a precarious top-heavy structure. Strategist Jim Welsh warns that while headline indices hover near records, beneath the surface a “Great Rotation” is underway as smart money exits mega-cap tech and flows into small-caps. The Russell 2000 is carving out a classic “saucer bottom,” recently breaking above 2500 resistance, though Welsh cautions that 40% of Russell constituents are unprofitable. The wealth effect dependency creates vulnerability—the top 10% of wage earners account for nearly 50% of consumer spending, leaving no backup plan if asset prices decline.

Potential Resistance: 7041.34; 7119.39

Potential Support: 6849.17; 6778.60

Intuitive Surgical: Growth Slowdown Sparks Selloff (546.76)

Current Trend: Bearish (Correcting) Market Sentiment: Disappointed

Intuitive Surgical stock plunged 6% Wednesday after pre-announcing Q4 results that showed slowing growth despite beating revenue estimates. The company reported preliminary Q4 revenue of $2.87 billion (vs $2.73B expected), up 19% year-over-year, with full-year 2025 revenue reaching $10.06 billion (+21%). Worldwide procedures grew 18% in Q4 (da Vinci +17%, Ion +44%), but this marked a slowdown from 19% full-year growth. More concerning, management forecasts 2026 procedure growth of just 13-15%, a significant deceleration. Ion system placements fell to 42 in Q4 from 69 in the prior year period. With the stock trading at 71x earnings, investors are questioning whether a premium valuation is justified for decelerating growth.

Potential Resistance: 547.0; 561.2

Potential Support: 521.3; 506.7

Commodities

Gold: Record Highs Above $4,640 (4,600)

Current Trend: Bullish (Consolidating) Market Sentiment: Positive

Gold hit all-time highs above $4,640 per troy ounce before entering a corrective consolidation phase, weakening below $4,600 late week on easing geopolitical tensions and USD strength. The precious metal clinched its second consecutive week of gains, supported by rising Fed rate-cut expectations following in-line but still-elevated CPI data (2.7% YoY) and mounting concerns over Fed independence. Trump’s stepping back from Iran military threats after receiving assurances that killings would stop reduced immediate safe-haven demand, but structural bullish drivers remain intact. Analysts are now openly discussing potential moves toward $5,000 given the combination of geopolitical uncertainty, sticky inflation that may force more Fed cuts, and the political pressure campaign against Powell.

Potential Resistance: 4718.63; 4830.74

Potential Support: 4473.76; 4355.75

WTI Crude Oil: Holiday Weekend Gains (59.44)

Current Trend: Mixed/Consolidative Market Sentiment: Cautious

WTI crude settled at $59.44 Friday (+0.5% for the week), while Brent finished at $64.13 (+1.2% weekly). Prices rose as some investors covered short positions ahead of the three-day Martin Luther King holiday weekend and on lingering worries about possible US military strikes against Iran. The USS Abraham Lincoln aircraft carrier was expected to arrive in the Persian Gulf this week, raising concerns about potential Strait of Hormuz disruptions. However, Trump’s de-escalation comments and expectations of higher global supply in 2026 are limiting the geopolitical risk premium. Oil markets remain caught between supply adequacy and tail-risk geopolitical scenarios.

Potential Resistance: 61.02; 62.99

Potential Support: 56.85; 54.84

Crypto

Bitcoin: Institutional Inflows Power Rally (95,500)

Current Trend: Bullish Market Sentiment: Positive

Bitcoin surged more than 5% for the week to hold above $95,500, supported by the strongest institutional demand in three months. Spot Bitcoin ETFs recorded net inflows of $1.81 billion through Thursday—the highest weekly inflow since early October when BTC reached its all-time high of $126,199. Corporate demand also remained robust, with Strategy Inc. purchasing 13,627 BTC, bringing total reserves to 687,410 BTC. Softening core CPI data (2.6% vs 2.7% expected) and improving risk sentiment as US-Iran tensions eased provided additional tailwinds. However, unexpected strength in Initial Jobless Claims (198K vs 215K expected) confirmed labor market resilience, reducing urgency for Fed cuts and causing mild pullback pressure. The delayed Senate crypto market structure bill continues to create regulatory uncertainty.

Potential Resistance: 99879.26; 106346.81

Potential Support: 89975.83; 84249.36

Key Events This Week (January 19–23, 2026)

Martin Luther King Jr. Day

- Monday: US markets closed for a holiday

Critical Data Releases

-

Tuesday:

Germany Current Account, Eurozone Sentix Investor Confidence, UK Employment Data (3 months to November) – key for BoE -

Wednesday:

UK December CPI – critical for BoE February decision, US Retail Sales (November) -

Thursday:

US PCE Price Index (October & November) – Fed’s preferred inflation gauge,

Q3 GDP revision, Weekly Jobless Claims, UK Monthly GDP, Industrial/Manufacturing Production -

Friday:

Global PMIs for January (S&P Global preliminary estimates for US, UK, Eurozone),

German ZEW Economic Sentiment

Davos Economic Forum (All Week)

- ECB President Christine Lagarde

- Multiple global policymakers and central bankers

- Key themes: Trade policy, inflation outlook, geopolitical risks

Fed Chair Speculation

Trump expected to announce Powell’s successor “soon,” with Kevin Hassett, Kevin Warsh, Christopher Waller, and Michelle Bowman as leading contenders. Markets are on high alert for any announcements, given implications for future monetary policy direction.

Bank of Japan Meeting

BoJ expected to stand pat, with focus on guidance after recent election reports.

Week Ahead Outlook

The week’s dominant narrative centers on concerns about Fed independence and speculation over Powell’s successor. Markets face a critical test on Thursday with the release of PCE inflation data — the Fed’s preferred gauge — which will heavily influence expectations for the January 28 meeting. Current pricing shows virtually no chance of a cut, with markets expecting about 45 basis points of easing for the full year.

UK data takes center stage Tuesday and Wednesday with employment figures and December CPI. The BoE’s dovish pivot by policymaker Taylor suggests the central bank may be positioning for more aggressive easing if inflation cooperates, potentially weighing on Sterling.

The political backdrop remains unprecedented. Powell’s public rebuke of the DOJ probe and the global central banking community’s solidarity statement underscore the gravity of the situation. Whether Trump nominates Hassett (seen as more dovish) or maintains a hawkish appointee could reshape currency markets and risk appetite dramatically.

Geopolitical tensions have eased modestly, with Trump stepping back from Iran military action and Netanyahu urging restraint. However, the USS Abraham Lincoln’s presence in the Gulf and ongoing Venezuela oil sector restructuring keep tail risks elevated for energy markets.

The “Great Rotation” from mega-cap tech into small-caps and quality stocks continues beneath the surface, driven by extreme concentration risk (41 AI stocks = 47% of S&P 500 value) and the precarious wealth effect. With the top 10% controlling roughly 50% of consumer spending, any sustained asset price decline could trigger a self-reinforcing downturn.

Risk management remains paramount given the toxic brew of political interference in central banking, sticky inflation, decelerating growth signals (Intuitive Surgical’s guidance), and a market structure increasingly dependent on a handful of AI winners. The coming week’s data and Davos commentary will be critical in determining whether recent equity strength can be sustained or if cracks are beginning to show.